It is Your Call Whether to Prevent Fraud Losses or to Say “Kiss It Goodbye”!

Fikret SebilcioğluThe fraud risk is not remote. Companies lose significant amount of money due to preventable fraud. Are you going to live with the threat of being hit by fraud or launch a counterattack?

Fraud prevention initiatives aim to minimize the likelihood of fraud occurring while maximizing the possibility of detecting any fraudulent activity. If the defense mechanism is well established, then perpetrators most often feel uncomfortable and get the feeling of being caught so that they are persuaded not to commit the fraud. From this perspective, it is clear that the existence of a thorough control system is a must to prevent fraud.

How to Sell Fraud Prevention to Management?

Usually the main issue is how to convince the management including board, to make an investment in these fraud prevention measures. Management may resist supporting that investment in such measures due to the various reasons including:

- Fraud may not concern management and they do not understand that fraud is hidden and that losses go undetected. They also may not recognize the fact that their employees can steal from their own companies. Simply, the management believes that fraud is not really a problem in the organization.

- The management may think that likely fraud incidents would not be costly to the organization.

- Managers may be reluctant to believe in the presence of fraud because of the hidden nature of fraud. If one employee is caught committing fraud, management may too often think that it is an isolated case and it is not worth putting too much effort to understand the root cause. Management eventually must understand that when instances of fraud are detected, it is too late to minimize the impact and recover the stolen assets.

- The management sometimes may feel that addressing the fraud subjects has a negative impact in the organization and this will make employees uncomfortable. The management should be reminded that normally employees appreciate working for an honest organization and they will definitely respect the management’s effort in fighting against fraud. This will in turn increase employee’s loyalty that is crucial component of business success.

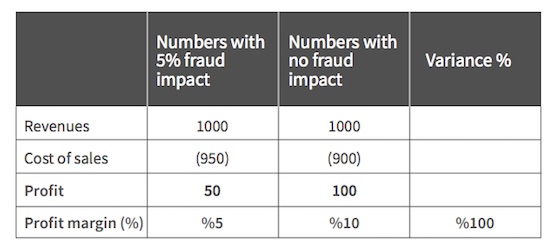

So how we can convince management to make investment in fraud prevention measures? Money is understandably the most important thing in business. Therefore, it may be wise to approach management by showing them how to make money and increase profits by preventing fraud. The easiest and most credible way to create this impact may be to show %5 fraud loss estimate that is calculated by ACFE. As stated in the 2018 ACFE report, the Certified Fraud Examiners who participated in the survey estimated that the typical organization loses 5% of revenues in a given year as a result of fraud.

Let’s analyze the following simple example. It reveals that if an organization prevents %5 loss on revenues, it is possible to increase net margin by some 100% if other elements remain same. I bet, showing this impact could definitely attract the management’s attention. Don’t forget to say, “Fraud can be very expensive”.

Another aspect of how to attract the attention of management over fraud prevention is the reputation risk. The management is often extremely sensitive to adverse publicity than almost any other issue. Therefore, pointing out that negative publicity may have a devastating impact on the bottom line in fraud cases could be an effective way of convincing executives to have a better understanding of the logic of fraud prevention. This negative impact can be eliminated or reduced by a proactive fraud prevention program.

After the challenge of persuading the management to act on fraud prevention, you are ready to take actions in your organization considering fraud risks specific to your organization and industry. At this stage the following procedures and mechanisms may help you design your own fraud prevention program:

- Proactive audit procedures

- Use of analytical review procedures

- Fraud assessment questioning

- Surprise audits where possible

- Code of conduct

- Internal audit department

- Employee anti-fraud educations

- Enforcement of mandatory vacations

- Job rotation policy

- Effective management oversight

- Reporting programs

- Increasing the perception of detection

- Tone at the top

- Organizational structure

- Background checks

- Performance management and measurement

- Handling of known fraud incidents

- A written anti-fraud policy

The cost and benefit analysis of investing in fraud prevention measures is very clear. It is much more cost effective to proactively address fraud risks than to suffer preventable fraud and spend valuable resources on detecting, investigating, prosecuting, and cleaning up after it. In other words, to prevent fraud from occurring directly increases the organization’s bottom line.

It is your call whether to prevent fraud or say “kiss it goodbye” by accept the loss of fraud!